Last week saw the fastest 10+% decline from a 52 week high in history. From peak-to-trough, the S&P 500 Index fell over 16% in 6 days. Additionally, all S&P 500 sectors declined 10% or more over the same period. This also occurred on a global scale, where every country’s stock market in the world has seen a sea of red. Even gold, precious metals, and commodities were being sold on widespread fears over the corona-virus.

“All things are subject to interpretation…whichever interpretation prevails at a given time is a function of power and not truth.”

-Friedrich Nietzsche

Portfolio Update – Is Everyone Awake Now?

It was a bloodbath last week, so let’s get right to the point. With the intensity of the latest decline, many records were broken. It was not pretty and (for the time being anyways), it will go down in the record books.

While we are caught up in the day to day volatility of the markets’ ups and downs, it is important that we also take a step back and remember that weeks like the one we just withstood is the primary reason we have built the processes we have around managing portfolios. Having a plan is so important during times of increased volatility, as these processes are put in place with the purpose of navigating through the markets, regardless of the backdrop. Having a process and plan before times like these are upon us is crucial in being able to come out the other side intact.

Part of our investment process that does not get used very often is recognizing when panic conditions exist. Various quantitative indicators we measure are designed to recognize severe and abnormal volatility. When certain criteria exists like it did last week, it is much better to not sell into the panic, and instead wait to re-evaluate as these conditions subside. The panic conditions are indeed starting to calm (at least for now), and we are now analyzing data on prudent next steps to take.

Although the severity and swiftness of the move was unprecedented, our strategies performed as expected. Here specific actions that we took for clients over the past few weeks:

- In early February, we sold all international and emerging market stock exposure and moved into long-term US Treasury bonds.

- There was an ETF that liquidated on February 14th, and was in cash prior to the move lower.

- Once the selloff began, we received sell signals on a few individual stocks, which increased cash across client portfolios.

- We sold high yield bond exposure one day after the selling began, further reducing risk.

- Following the third day of selling (that included two 1000-point down days and one 800-point down day on the Dow), our panic signals kicked in and advised us to stop making additional sells.

- By last Friday, we began adding stock exposure as well as repurchase some existing holdings near the bottom of this move.

- We also rotated out of some stocks that weren’t working well and into others that were showing more resilience and better opportunity.

Overall, we have been very pleased with how our strategies performed through all the volatility. (If you have specific questions on your account, please do not hesitate to reach out as always).

However, we are still concerned about what may happen next.

It appears as though the risks and uncertainties around the corona virus are to blame for the recent selloff. At this point, we do not think it is prudent to try to understand all the possible outcomes of what the corona virus may do. We only know that there are very bad scenarios, yet also some not-so-bad ones.

The main problem we see with diagnosing the virus outcomes is simple…what should we believe? The number of cases globally could be massively understated, as there are simply not enough testing kits to possibly test everyone who has symptoms. Also, there could be millions with the virus that are asymptomatic, or not showing any symptoms right now.

Would that be good or bad? It would be bad in that it would likely increase the panic surrounding the virus. But it may also be good in that it could make the actual mortality rate much lower than it appears now, and possibly less fatal than the flu.

Those in power across the globe are determining what information is appropriate to disseminate, and we can’t help but be skeptical about what are actual facts.

It would be difficult enough to predict how the virus may or may not spread. Trying to then predict how markets will respond to a potentially endless number of scenarios is infinitely more complex. Add to that uncertainty around the actual data, and there is a recipe for prediction disaster.

We have said many times that we simply don’t care why the market is doing what it is doing. We simply want a plan on how to handle what happens.

We want to understand the landscape and potential impacts, and we continue to monitor a variety of risks very closely. But ultimately it doesn’t matter why. This is why we rely on a process, not guesswork.

Which brings us to simply analyzing what “is” in the market right now.

First Correction since 2018

The S&P 500 fell over 16% from peak to trough in only 6 trading days. Since the decline exceeded 10%, we now have seen the first market correction since the 4th quarter of 2018. Let’s look at some of the unique characteristics of this latest fall from grace and where we may be headed from here.

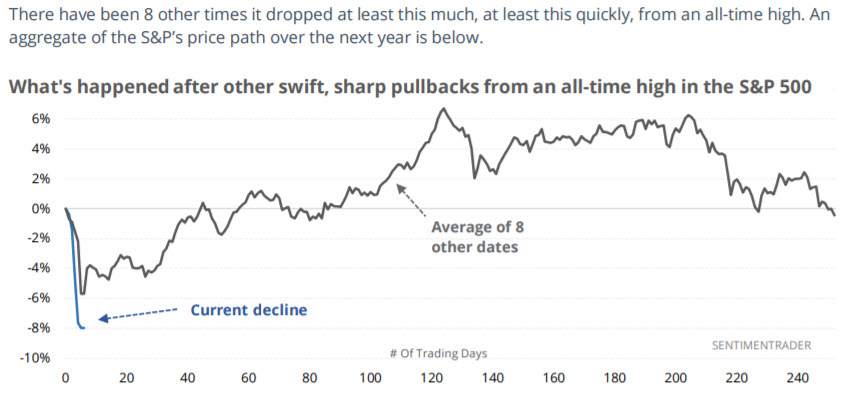

The first chart below (courtesy of Bloomberg and LPL) shows just how swift this was compared to other 10% drawdowns. Officially it was the fastest decline of 10%+ from an all time high on record since the S&P 500 Index began on March 4, 1957.

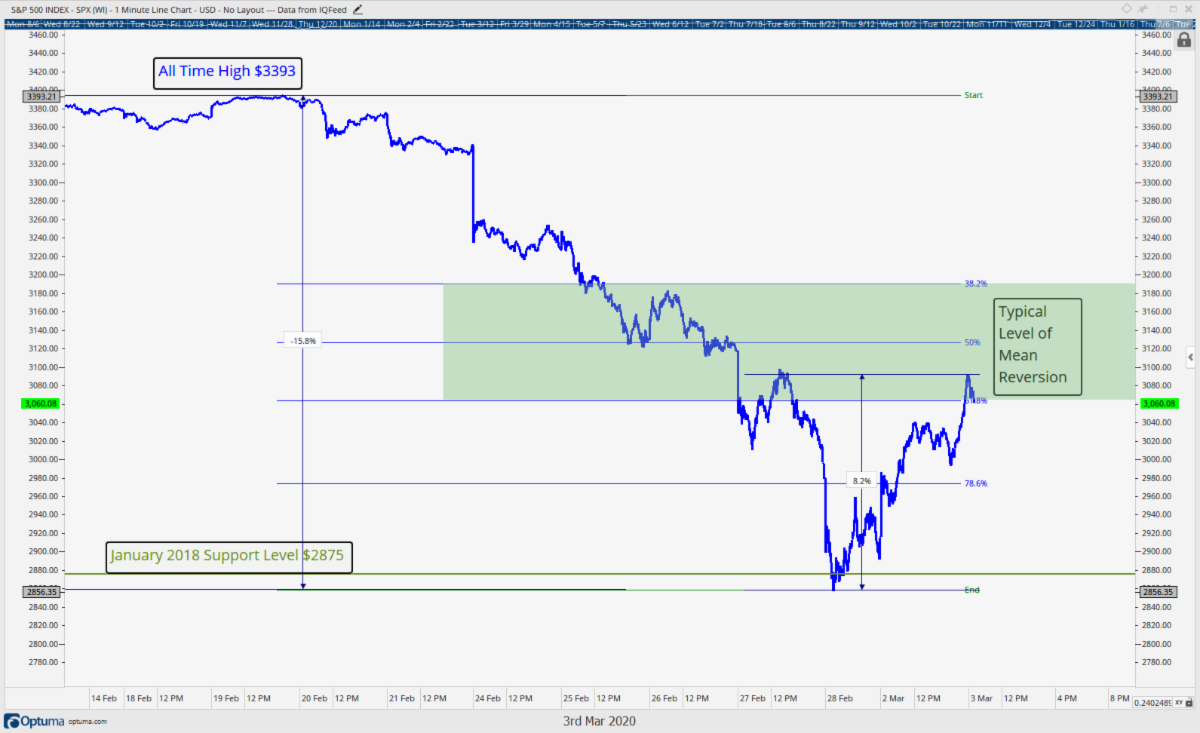

This took prices all the way back to January 2018’s top (SPX 2875). At one point during this recent decline, 2 years of gains were wiped out.

This took prices all the way back to January 2018’s top (SPX 2875). At one point during this recent decline, 2 years of gains were wiped out.

The chart below shows that reality.

Do you think those January price levels are important? You bet they are! This is the quintessential definition of support and resistance levels. January 2018’s previous resistance has now become February 2020’s support. This is a key level to watch if selling resumes.

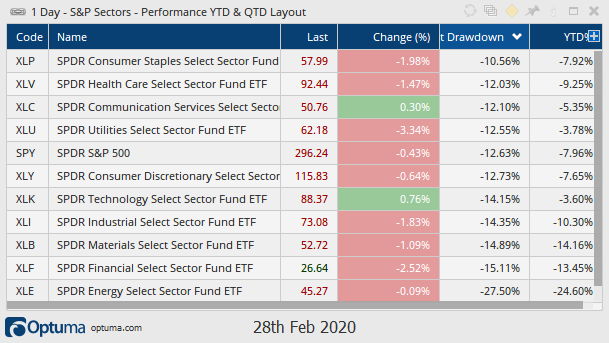

Another unique characteristic of this decline is just how widespread it was. The decline touched every single S&P 500 sector in a very negative way, offering up a little humble pie to those who rely solely on diversification to protect their portfolios from “risk”. Even the typically less volatile sectors (Consumer Staples and Healthcare) were down more than 10%. The drawdown column in the below chart shows the decline of each sector from their recent 52 week highs. Staples fell 10.56% while Energy was down a whopping 27.50%

In a week where Treasury bonds skyrocketed, it is inconceivable that Utility stocks, with the highest correlation to Treasuries and the lowest correlation to the S&P 500, still fell 12.5%! Yet, these are events we just witnessed and goes to show you cannot depend on diversification to protect you in the event of a stock market decline. If nothing else it’s likely a testament to just how stretched we had gotten on the upside.

They say that the four most dangerous words in investing are “this time is different”, yet time and time again we find unprecedented

and “different” events occurring in the markets. We think largely that quote is meant for higher level behavioral finance concepts, like fear and greed always being present in the markets; not for in-the-weed statistics like the ones above, but it’s hard to argue with the fact that actually, yes, this selloff was different.

An example of how this time was “different” was that diversifying your portfolio alone did not help you during last week’s slaughter (this is quickly becoming a common theme during selloffs). This is one reason why our strategies don’t rely solely on diversification to protect during drawdowns.

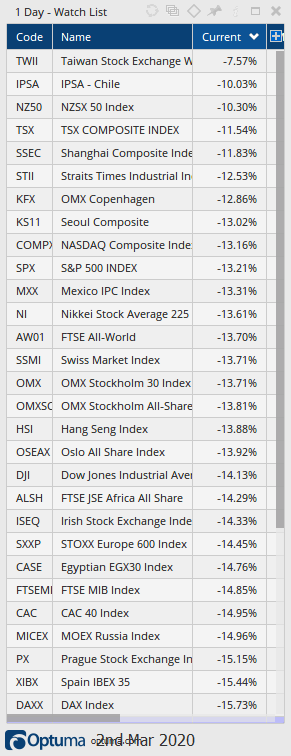

In the next chart below, international stocks also showed how widespread the selling was and how little diversification did for your portfolio. As of Monday, March 2, Every major stock market in the world had significant price drawdowns from their highs, with many down 15% or more. The median drawdown was 14.41% across the world over the last few weeks.

Another interesting aspect, and another continued knock on modern portfolio theory, the S&P 500 continues to massively out-perform the other markets around the world, even with its significant decline in February.

Anyone Hear the All-Clear Siren?

So are we all clear? Is the selloff over? If this decline is like most of the recent ones, then it would not be difficult to assume that yes, this decline is now over. The chart and statistics below, courtesy of SentimentTrader.com suggests that generally, after such a swift pullback in the markets, stocks are up over the next 6 months.

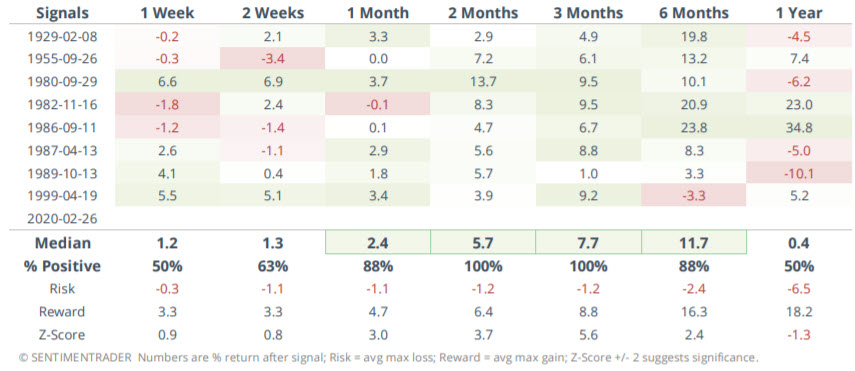

The chart and table below show the results from the other times the market fell so quickly from its all time highs. Of note, though, is one year later the average return has been flat, so that’s certainly a possibility. In addition and shown in the table, there are less than 10 data points, not near enough to try to make a statistically based gamble on the direction of the market, but if we were to accept these examples as representative then it would be safe to say we could be 1-12% higher in 6 months with a big risk we retest the lows within a year (note: we are already 5% higher after Monday’s, 3/2/2020, rally).

Other Times the Market Fell This Swiftly from an All Time High

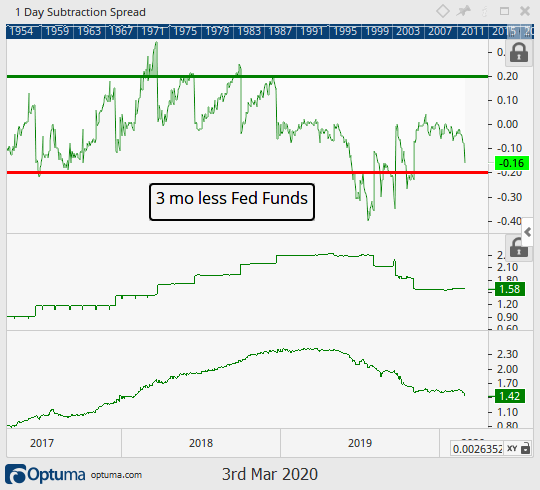

Additionally, on Tuesday, March 3, the Federal Reserve also tried to come to the market’s rescue as it did its first “surprise” rate cut since 2008, a 50 basis point cut “in order to get ahead of the potential economic disruptions resulting from the Corona Virus”. This was a major surprise and the market initially liked it, up 1% on the news, but then immediately gave back all those gains and then some closing down over 2%.

Our Fed Monitor suggests this was an unnecessary move by the Fed and only means they have less ammo if a recession does eventually develop and they need to cut the remaining 1%. Our Fed Monitor is shown below through last week and reveals the 3 month Treasury rate has not really moved that much during the last month (while the longer end of the Treasury curve has been tanking). Based on our model, the Fed Funds rate was only 16 basis points above the market’s 3 month Treasury yield, right in the historical normal range between + or -20 basis points. This latest Fed move puts them near a historically low 30+ points below the market rate. It seems they may have reached for this one.

Nevertheless it is just another data point that the Fed “has the market’s back” as global central bankers continue to do all they can to keep the bull raging.

Looking Forward

What if this decline is like 1987 or 1989 or 1999, when the market saw further declines following such swift corrections from an all time high? After all, and shown in the table above, 3 of the 8 other times this occurred saw the correction fall further at some point within the next year.

The good news is we don’t have to try to guess if that will be the case. That’s one of the luxuries of having a process-driven portfolio management system. We are prepared for either outcome and we don’t have to guess what the market will do next. Besides being impossible to do, guessing what the market will do leaves a manager relying solely on luck rather than skill in navigating the markets.

If this decline is like all the other recent ones and wants to “V” bottom here (a term given to a swift decline that is immediately followed by a swift rally due to its shape of a “V” as viewed on a chart), then our client portfolios are already prepared for such outcomes.

However, if “this time is different”, and the recent decline does not hold, we have our strategies in place that will, once again, have us moving into safety and raising cash as necessary, just as they were designed to do.

On Monday, March 2, the Dow rallied the most points in its history, up over 5%, gaining back some of last week’s losses, but then those gains were half given back on Tuesday, March 3. So where do we go from here?

If you have followed our research for awhile you may remember a piece we put out entitled, “What does a Market Top Look Like?” In it we recognized a few technical readings that seemed to appear during topping processes. One of those is an initial decline that is followed by a bounce into a key resistance zone.

Right now that resistance zone is in the range of 3050 to 3120, where prices are trading as we go to print, so we are right in that first area of resistance. A rejection in price at this level, followed by a resumption of the downtrend back below last week’s and January 2018’s price high (discussed earlier) would be a bearish event and similar to other major tops that have occurred during our lifetime.

However, if price can continue to move higher from here, through the green shaded area and above the 3260 level, it is likely we have ourselves another “V” bottom, and we should look for new all time highs once again.

Invest Wisely!

Our clients have unique and meaningful goals.

We help clients achieve those goals through forward-thinking portfolios, principled advice, a deep understanding of financial markets, and an innovative fee structure.

Contact us for a Consultation.

Neither the information provided nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. The investments and investment strategies identified herein may not be suitable for all investors. The appropriateness of a particular investment will depend upon an investor’s individual circumstances and objectives. *The information contained herein has been obtained from sources that are believed to be reliable. However, IronBridge does not independently verify the accuracy of this information and makes no representations as to its accuracy or completeness. Disclaimer This presentation is for informational purposes only. All opinions and estimates constitute our judgment as of the date of this communication and are subject to change without notice. > Neither the information provided nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. The investments and investment strategies identified herein may not be suitable for all investors. The appropriateness of a particular investment will depend upon an investor’s individual circumstances and objectives. *The information contained herein has been obtained from sources that are believed to be reliable. However, IronBridge does not independently verify the accuracy of this information and makes no representations as to its accuracy or completeness.